What to Do If You Default on Your IRS Installment Agreement (Notice CP523)

Everything is going well. You have your IRS tax debt under control through an installment agreement. Then, unexpectedly, a letter arrives from the IRS: Notice CP523, Intent to Terminate Your Installment Agreement.

The notice demands immediate action, and your first thought may be: “How did this happen, and what can I do now?”

Fortunately, receiving a CP523 does not necessarily mean your installment agreement is over. In many cases, we have options to cure the default and file an appeal to reinstate our agreement, or negotiate a new resolution with the IRS.

What Causes IRS Installment Agreements to Default?

The IRS defaults agreements for a variety of reasons, but the most common reasons are either (1) missing a payment on your current installment agreement, or (2) failure to pay another tax liability when it was due.

Most of my clients are surprised to learn that any new balance owed for a new tax year will default your current agreement. This includes new balances from interest or penalties on your most recently filed return. The IRS cannot bill you for anything, even one dollar, or you risk a default on your current installment agreement.

For example, if you file your current year taxes with an extension until October 15, when you file the IRS says you owe $10,000, which you promptly pay. However, the extension you filed was an extension to file, not pay, so the IRS assessed a small failure to pay penalty against you. This could cause your agreement to default if these penalties are not paid when the return is filed.

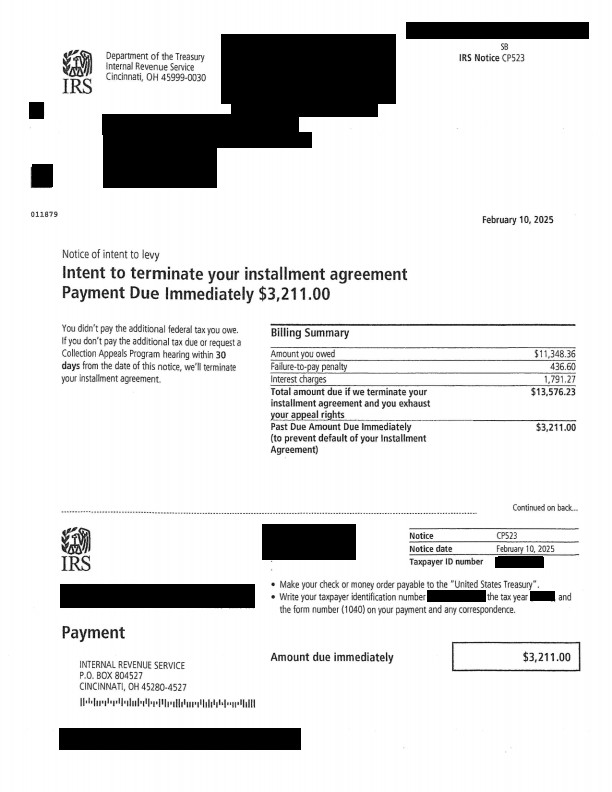

A CP523 will look like this:

What can I do?

The Internal Revenue Manual and supporting law give us a clear path to restoring our agreement.

First, installment agreements are authorized under Internal Revenue Code Section 6159. This section authorizes taxpayers to make installment payments on liabilities. The secret to an installment agreement termination is in IRC 6159(b)(5). This section states that the IRS must notify us at least 30 days before they cancel our agreement. This is why you received the CP523 in the mail. It is your 30-day notice.

Additionally, the code section works in tandem with the Internal Revenue Manual (IRM) specifically, IRM 5.14.11.5 and 5.1.9.4.2(19)(c). These manual provisions provide that we have 30 days to request an appeal to reinstate our agreement. The provisions provide that within 30 days, the taxpayer should cure the balance owed or the installment agreement will default. It is important that the amount stated on the letter be cured. Without payment, the IRS may be hesitant to reinstate your agreement.

What if I Cannot Cure my Payment?

If your financial situation has changed, or your cash flow is tight for the foreseeable future, we have alternative options for the installment agreement. First, we must assess where your file is with the IRS. Is your file with the IRS’s automated collections? Has the IRS issued a Final Notice of Intent to Levy? Has the file been assigned to an IRS Revenue Officer? These factors can determine what our next steps are.

For example, if we had previously disclosed financials using IRS Form 433-A with a Revenue Officer, and they placed us in an installment agreement, when the agreement defaults the file usually returns to the Revenue Officer. At that point, we could renegotiate payment terms that better fit your current financial condition.

Likewise, if you negotiated an installment agreement with IRS collections, we can go back and renegotiate. We can always go back and renegotiate with IRS collections. Sometimes, I find that an IRS streamlined agreement can be a lower monthly payment than a regular financial disclosure.

While receiving an IRS CP523 can be alarming, it is not the end of the road. The notice is intended to provide us with an opportunity to address the issue before the IRS terminates our installment agreement.

How we can Help.

We regularly assist taxpayers with their CP523 Notices. We can assist by either securing new installment agreement, or reinstate your existing ones.